Getting a loan used to be a long process that required waiting, a lot of paperwork, and several trips to the bank. Borrowers often dealt with delays, poor communication, and complicated eligibility requirements. In 2025, digital lending platforms changed how individuals and businesses get credit. Today, instant digital loans are available, and paperless loan processes provide smooth and efficient borrowing experiences.

The rise of digital lending in India is not just a change in technology; it represents a fundamental shift in the financial system. Small businesses in Tier-2 cities and salaried professionals in urban areas now have access to personalized, fast, and secure loans. Knowing about digital lending in 2025 is important for anyone dealing with credit, whether for personal, business, or investment needs.

Example: A freelance designer in Jaipur can now secure a quick personal loan online within hours to cover urgent expenses, leveraging a platform that assesses creditworthiness through AI and digital transaction history, without the need for collateral.

What is Digital Lending?

Digital lending is the process of providing loans online. It uses technology and data to assess creditworthiness, speed up approvals, and manage repayment cycles. Unlike traditional loans, which often need extensive paperwork and in-person meetings, digital lending provides a seamless experience for both borrowers and lenders.

Key elements of digital lending include:

- Online loan platforms: Applications, approvals, and repayments happen entirely online.

- AI-driven credit evaluation: Sophisticated algorithms assess risk and eligibility.

- Automation: From KYC verification to fund disbursal, most steps are automated.

- Paperless loan process: Eliminates manual documentation, reducing delays and errors.

Digital lending is a crucial component of modern fintech lending solutions, enabling faster, safer, and more inclusive credit distribution.

Evolution of Digital Lending in India

The journey of lending in India has evolved from traditional bank-centric models to fully digital ecosystems.

- Traditional Banking Era: Loans were accessible primarily to urban populations with established credit histories. Paperwork was extensive, approvals were slow, and accessibility was limited.

- Fintech Emergence (2010–2020): Startups began offering personal loans online with minimal documentation. Integration with digital payment systems, mobile apps, and UPI laid the groundwork for faster loans.

- Post-Pandemic Growth (2020–2025): COVID-19 accelerated the adoption of online loan platforms. Remote work, digital payments, and widespread smartphone penetration drove the shift to fully paperless loans.

Key statistics supporting the evolution:

- India had 881 million internet subscribers by March 2023.

- Smartphone users are expected to reach 1 billion by 2026, supporting mobile-first lending.

- India’s digital consumer lending market is projected to cross $720 billion by 2030, with digital lending accounting for 55% of this growth.

This growth demonstrates the increasing importance of digital lending platforms and quick personal loans online as part of India’s financial landscape.

Read More: Check your eligibility and apply for an instant personal loan online in just a few minutes!

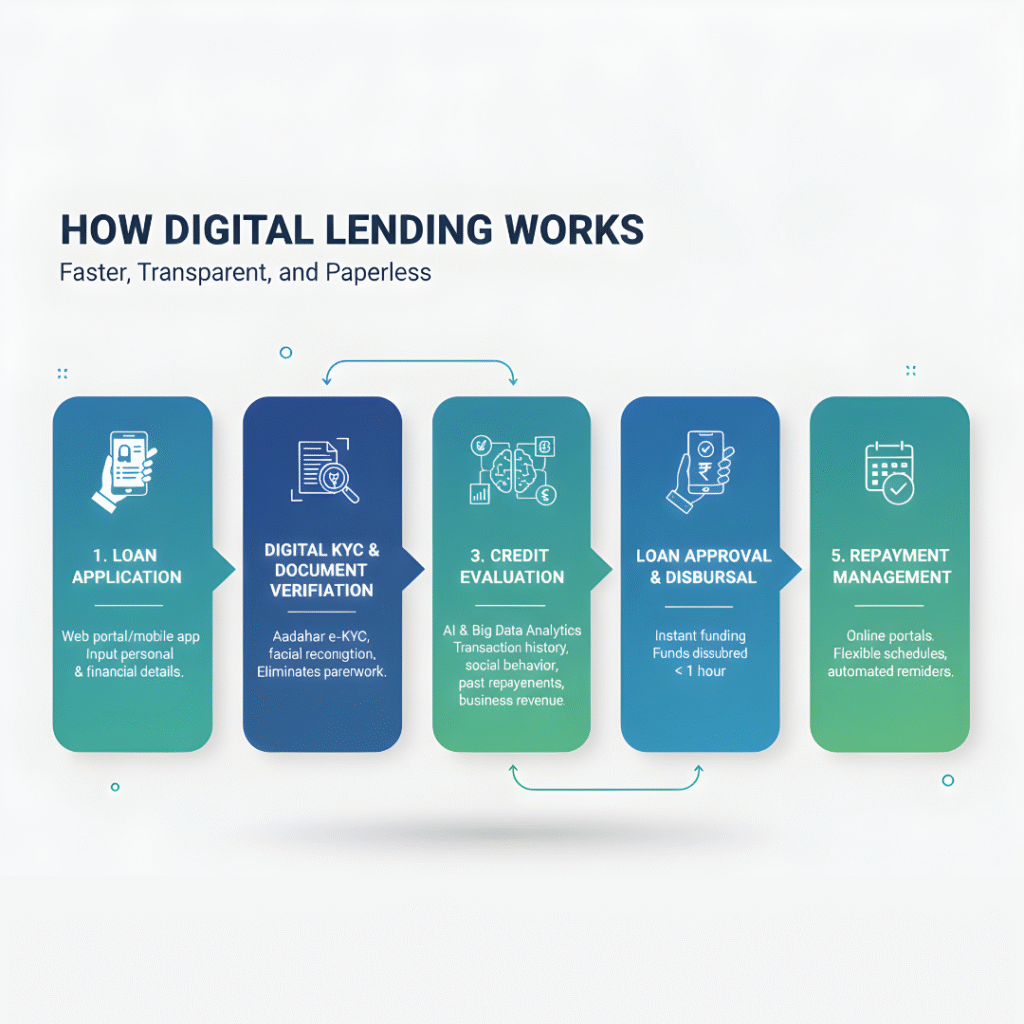

How Digital Lending Works?

The process of obtaining a loan via digital lending platforms is significantly faster and more transparent than traditional methods. Here’s a detailed breakdown:

1. Loan Application

Borrowers initiate a request via a web portal or mobile app. These online loan platforms allow users to input basic personal and financial details.

2. Digital KYC & Document Verification

Identity verification is conducted digitally. Platforms may use Aadhaar e-KYC, facial recognition, or government-backed databases. This ensures compliance with regulatory standards while eliminating paperwork.

3. Credit Evaluation

AI and big data analytics evaluate the borrower’s creditworthiness. Algorithms may consider:

- Transaction history

- Social behavior patterns

- Past credit repayments

- Business revenue streams (for SMEs)

This allows lenders to offer personal loans even to individuals with minimal or no traditional credit history.

4. Loan Approval & Disbursal

Once verified, funds are disbursed instantly. Instant digital loans are a hallmark of modern digital lending in India, with approvals sometimes taking less than an hour.

5. Repayment Management

Borrowers can manage repayments online, with flexible schedules and automated reminders. The paperless loan process ensures transparency and convenience.

Example: A freelancer needing ₹75,000 for equipment upgrades could secure a personal loan online within two hours, thanks to automated credit evaluation and digital disbursal.

Key Technologies Powering Digital Lending

Modern digital lending platforms leverage several cutting-edge technologies:

- Artificial Intelligence & Machine Learning: For predictive credit scoring and risk management.

- Big Data Analytics: Analyzing transaction data, spending patterns, and repayment behavior to make better loan decisions.

- API Infrastructure: Seamless integration with banks, payment gateways, and verification systems.

- Blockchain (Emerging): Ensures transparency, prevents fraud, and supports secure paperless loan processes.

These technologies collectively support quick personal loans online, reduce operational costs, and improve borrower experience.

Types of Lending Models

Digital lending has changed into several models, each aimed at meeting different borrower needs and market segments. Knowing these models helps borrowers pick the right platform and lets lenders focus on the right audience effectively.

1. Traditional Bank-Led Digital Lending

- Description: Banks digitize their conventional loan processes, offering services through web portals and mobile apps. These platforms combine regulatory oversight with modern technology.

- Key Features: Full compliance with RBI regulations, moderate interest rates, and access for established credit history holders.

- Best For: Salaried professionals or borrowers with a strong credit history seeking secure and regulated personal loans.

- Example: HDFC Bank and ICICI Bank offering personal and business loans via their digital portals.

2. Peer-to-Peer (P2P) Lending

- Description: Connects borrowers directly with individual lenders, bypassing traditional banks. Interest rates can be more flexible and competitive.

- Key Features: Flexible terms, alternative credit scoring, and often lower eligibility requirements.

- Best For: Individuals or small businesses who may not qualify for traditional loans but have a reliable repayment plan.

- Example: Faircent or Lendbox in India providing P2P platforms for small loans and short-term credit.

3. Neo Banks & Fintech Lenders

- Description: Digital-only banks or fintech companies offering quick personal loans online with minimal documentation.

- Key Features: AI-driven credit evaluation, instant approvals, and paperless disbursal.

- Best For: Millennials, freelancers, and small business owners seeking instant digital loans and a fully mobile-first experience.

- Example: KreditBee or CASHe providing tailored loans for salaried professionals and freelancers.

4. Embedded Lending (BNPL, SME Financing)

- Description: Loans integrated directly into e-commerce platforms, marketplaces, or business services. Includes Buy Now, Pay Later (BNPL) and working capital for SMEs.

- Key Features: Seamless experience at point-of-sale, often instant disbursal, repayment linked to transaction history.

- Best For: Online shoppers using BNPL options or small businesses needing short-term operational capital.

- Example: ZestMoney (BNPL) and LendingKart (SME working capital financing).

5. Microfinance Digitization

- Description: Focuses on underserved populations or rural borrowers. Digital tools reduce paperwork and increase reach.

- Key Features: Small loan amounts, simplified eligibility, often no collateral required.

- Best For: Low-income individuals, rural entrepreneurs, or women-led micro-enterprises seeking small but impactful loans.

- Example: ESAF or SKS Microfinance using digital platforms to streamline rural lending.

Comparison Table: Which Model Suits Whom

| Lending Model | Target Borrowers | Loan Type | Key Advantage | Ideal Use Case |

| Traditional Bank-Led Digital Lending | Salaried professionals, established borrowers | Personal, Home, Business | Regulated, secure | Large personal loans, long-term financial planning |

| Peer-to-Peer Lending | Individuals & small businesses with limited bank access | Short-term, small personal/business loans | Flexible terms, lower interest | Freelancers, new businesses |

| Neo Banks & Fintech Lenders | Millennials, freelancers, tech-savvy borrowers | Personal loans, instant credit | Instant approval, fully digital | Urgent small loans, lifestyle financing |

| Embedded Lending (BNPL/SME) | Online shoppers & SMEs | Point-of-sale credit, working capital | Seamless, integrated | E-commerce purchases, SME cash flow support |

| Microfinance Digitization | Rural, low-income borrowers | Small personal/business loans | Accessibility, minimal paperwork | Women entrepreneurs, rural small businesses |

Looking for quick access to funds? Discover the best apps to get an instant personal loan online fast, secure, and right from your smartphone.

Digital Lending vs Traditional Lending

| Factor | Digital Lending | Traditional Lending |

| Application | Online, paperless | In-person, paper-heavy |

| Credit Check | AI/Data-driven | Credit bureau-based |

| Approval Time | Minutes to 24 hrs (instant digital loans) | Days to weeks |

| Accessibility | Wide, including new-to-credit borrowers | Limited to established customers |

| Cost Efficiency | Lower operational cost (fintech lending solutions) | High infrastructure cost |

Digital lending clearly offers faster, more inclusive, and cost-effective solutions compared to traditional loans.

Benefits of Digital Lending

Digital lending platforms offer tangible benefits for individuals and businesses:

- Speed & Efficiency: Access quick personal loans online in hours.

- Smarter Risk Assessment: AI-driven evaluation improves approval accuracy and minimizes defaults.

- 24/7 Accessibility: Apply anytime from anywhere through online loan platforms.

- Financial Inclusion: Brings credit to rural and underserved populations.

- Sustainability: Reduces paperwork and branch dependency, promoting environmentally-friendly finance.

Example: A small SME in Jaipur secured a ₹2 lakh personal loan online to purchase inventory within three hours, a process that previously would have taken weeks.

Challenges in Digital Lending

While digital lending in India presents significant opportunities, challenges persist:

- Fraud & Cybersecurity: Digital systems are targets for scams and attacks.

- Data Privacy: Sensitive borrower information must be safeguarded.

- Customer Awareness: Not all users are familiar with online loan platforms.

- Regulatory Compliance: Evolving guidelines require constant updates.

- Technological Dependence: Reliable internet and devices are necessary for seamless borrowing.

Insight: These challenges are opportunities for innovative fintech lending solutions, smarter algorithms, and improved digital literacy campaigns.

The Potential of Digital Lending in India

Digital lending platforms are a catalyst for inclusive economic growth:

- Financial Inclusion: Bridging rural-urban gaps with accessible paperless loans.

- SME Empowerment: Enables faster working capital access, fueling entrepreneurship.

- Economic Growth: Supports sectors like EV financing, education, healthcare, and renewable energy.

Forecast: EV financing could represent a ₹1 lakh crore opportunity by 2028, highlighting the transformative impact of digital lending in India.

The Future of Digital Lending (2025 & Beyond)

The future is bright for digital lending platforms:

- Generative AI & Predictive Analytics: Smarter credit decisions and personalized loans.

- Blockchain & Secure Identity Verification: Fraud prevention and transparency.

- Open Banking & Alternative Scoring: Enables financial inclusion for previously underserved segments.

- Regulatory Evolution: Clearer RBI guidelines and compliance frameworks.

Human Impact: Digital lending will make finance faster, fairer, and more inclusive, empowering both individuals and businesses.

Key Takeaways

- Digital lending is revolutionizing finance through speed, efficiency, and inclusivity.

- AI and data-driven insights improve risk assessment and decision-making.

- Fintech lending solutions enhance access to personal loans and business capital.

- Paperless loan processes reduce costs and increase operational efficiency.

- The future of digital lending in India promises continued growth, financial inclusion, and innovation.

Conclusion

Digital lending in India is more than a trend. It represents a fundamental shift in how individuals and businesses access credit. Online loan platforms, instant digital loans, and paperless loan processes have made borrowing faster, more accessible, and more transparent. As technology keeps advancing, digital lending platforms will play a key role in promoting financial inclusion, empowering SMEs, and shaping the future of India’s financial ecosystem.

Explore digital lending platforms today and experience the convenience of instant digital loans. Whether for personal or business needs, embrace the future of finance with innovative fintech lending solutions and a completely paperless loan process.

MoneyBeing Private Limited – Trusted Loan Services in Jaipur & Across India

MoneyBeing Private Limited, founded in 2023 and headquartered in Jaipur, Rajasthan, is a leading financial solutions provider in India. As an official channel partner to top banks and NBFCs, MoneyBeing connects borrowers with reliable lenders, offering a seamless way to access personal loans, home loans, car loans, education loans, and other financial products online.

Wide Range of Loan Services

MoneyBeing specializes in tailored loan services in Jaipur and across India, meeting the diverse financial needs of individuals and businesses:

- Home Loans – Starting at 7.35% interest for property purchase, house construction, renovation, top-ups, and balance transfers.

- Personal Loans – From 10.5% interest, unsecured loans for personal expenses including marriage, travel, medical emergencies, and other flexible uses.

- Car Loans – Financing for new and used vehicles with rates from 7.75%, quick approval, and refinancing options.

- Education Loans – Loans starting at 8% for tuition, books, living expenses, and studies in India or abroad.

- Business Loans – Unsecured business loans, working capital, expansion funding, equipment loans, and loan against property starting at 8.35%.

- Specialized Products – Overdraft facilities, credit cards, and customized solutions for professionals like doctors and chartered accountants.

Why Choose MoneyBeing for Personal Loans Online India?

- Customer-Focused Solutions: Designed for salaried professionals, entrepreneurs, first-time borrowers, and seasoned investors.

- Pan-India Coverage: Digital-first services for clients in major cities and remote areas.

- Expert Guidance: Financial advisors help with loan selection, eligibility optimization, and compliance.

- Transparent Operations: No upfront fees; all applicable charges are handled directly by partner banks.

Simple Online Application

Borrowers can apply online by selecting loan types, entering location details, scheduling consultations, and receiving personalized loan recommendations.

With its focus on reliable loan services in Jaipur and across India, MoneyBeing Private Limited empowers borrowers to access fast, transparent, and customized financial solutions, making borrowing easier than ever.

Frequently Asked Questions (FAQs) – Digital Lending

Digital lending uses technology to evaluate, approve, and disburse loans online. Borrowers can apply via web or mobile apps, complete digital KYC, and get instant digital loans, all without physical paperwork.

Unlike traditional lending, which is paper-heavy and time-consuming, digital lending is online, automated, and faster. Borrowers benefit from quick personal loans online, lower operational costs, and flexible repayment options.

Digital lending services are accessible to salaried professionals, self-employed individuals, small business owners, and underserved populations. Many platforms provide quick personal loans online, even for borrowers with limited or no prior credit history.

Many fintech lenders assess alternative data, like income, transaction history, and UPI payments, allowing borrowers with low or no credit score to access personal loans online.

Yes, regulated platforms comply with RBI guidelines, ensure secure data encryption, and integrate fraud detection systems. Fintech lending solutions follow strict standards to protect borrower information.

Digital lending options differ in interest rates, loan amounts, processing speed, repayment flexibility, and eligibility criteria. Compare platforms based on customer reviews, regulatory compliance, and features such as paperless loan processes and instant disbursal.

Yes, most digital lending platforms allow early repayment. Some may offer incentives or lower interest for early closure, making borrowing more flexible compared to traditional loans.

Individuals needing urgent funds, freelancers, small business owners, and underserved populations benefit most. Digital lending platforms provide fast, accessible, and flexible loan options.

Key technologies include AI and machine learning for credit scoring, big data analytics for risk assessment, API infrastructure for instant verification and disbursal, and emerging blockchain solutions for security and transparency.